ఇన్కం ట్యాక్స్ రిటర్న్ ఇ-ఫైలింగ్ చేయడం:

పన్ను వర్తించే ఆదాయం రూ.2,50,000 కన్నా ఎక్కువ ఉన్న వారు జులై 31 లోగా

ఆదాయపు పన్ను రిటర్న్ దాఖలు చేయవలసి ఉంటుంది.

ఫిబ్రవరి మాసంలో సమర్పించిన ఫారం 16 ఆధారంగా రిటర్న్ దాఖలు చేయాలి.

దాఖలు చేయవలసిన విధానం:

వేతనం లేదా పింఛను ద్వారా ఆదాయం పొందుచున్న వారు, పెట్టుబడులపై వడ్డీ ఆదాయం పోన్స్య్ వారూ, ఒకే గృహం ద్వారా ఆదాయం ఉన్న వారు ITR-1(సహజ్) ఫారం ద్వారా రిటర్న్ దాఖలు చేయాలి.

ఆన్ లైన్ ద్వారా "ఇ- రిటర్న్" ను సులభంగా దాఖలు చేయ వచ్చు. దాఖలు చేసే విధానాన్ని పరిశీలిద్దాం.

పేరు రిజిస్టర్ చేసుకొనుట:

incometaxindiaefiling.gov.in వెబ్సైట్ ఓపెన్ చేసి Register your self అను ఆప్సన్ ను ఎంచుకొనవలెను. దానిలో పాస్ వర్డ్ తదితర వివరములను పూర్తిచేసిన తదుపరి మెయిల్ కు వచ్చిన లింక్ కాపీ చేసి బ్రౌజర్ లో పేస్ట్ చేసిన తర్వాత మొబైల్ కి వచ్చిన పిన్ నంబర్ ను నమోదు చేస్తే రెజిస్ట్రేషన్ పూర్తి అయినట్లే. మీ పాస్ వర్డ్ ను జాగ్రత్తగా ఉంచుకోవాలి.

ఫారం 26 AS:

ఇ- ఫైలింగ్ చేసేందుకు ఫారం 26 AS ను పరిశీలించుకోవాలి. పైన తెలిపిన వెబ్సైట్ ఓపెన్ చేసిన తదుపరి 'VIEW FORM 26 AS' ను ఎంచు కోవాలి. దానిలో యూజర్ ID అంటే పాన్ నంబర్, రిజిస్ట్రేషన్ లో మనం ఎంచుకొన్న పాస్ వర్డ్ తదితర అంశాలను నమోదు చేసిన తదుపరి ఫారం 26 AS ను క్లిక్ చేసి ఎసెస్మెంట్ సంవత్సరం సెలెక్ట్ చేసుకోవడం ద్వారా ఫారం 26 AS ఓపెన్ అవుతుంది. దానిలో ఆ సంవత్సరం మనం చెల్లించిన పన్ను సక్రమంగా నమోదు అయినదీ లేనిదీ పరిశీలించుకోవచ్చు. ఫారం లో పన్ను నమోదు సక్రమంగా ఉన్నప్పుడే ఇ- రిటర్న్ చేయాలి.

ఫారం 26 AS లో నమోదుల పరిశీలన:

ఫారం 26 AS లో మనం పరిశీలన చేసినప్పుడు మనం చెల్లించిన పన్ను సక్రమంగా నమోదు కానట్లయితే DDO కు తెలియజేయాలి. సక్రమంగా నమోదు కాక పోవడానికి కారణాలు DDO త్రై మాసిక రిటర్న్(Q1, Q2, Q3, Q4) లను సమర్పించక పోవడం లేదా సమర్పించిన వానిలో పొరబాటు జరగడం అయివుండ వచ్చు. త్రైమాసిక రిటర్న్ దాఖలు చేయవలసిన బాధ్యత DDO లదే కాబట్టి వారే దాఖలు చేయడం లేదా తప్పులను సవరించడం చేయవలసి ఉంటుంది.

ఇ- ఫైలింగ్ చేయడం:

ఫారం 26 AS లో పన్ను నమోదు సక్రమంగా ఉన్నట్లు సంతృప్తి చెందిన తరువాత ఇ- ఫైలింగ్ చేయడం ప్రారంభించాలి. ముందు చెప్పిన వెబ్సైట్ ఓపెన్ చేసిన తరువాత 'Quick e file ITR- 4S' ఎంపిక చేసుకోవాలి.

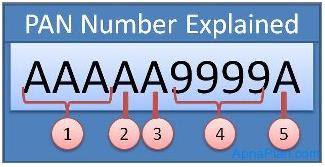

PAN నంబర్, పాస్ వర్డ్, పుట్టిన తేదీతడితర వివరాలను నమోదు చేసి లాగిన్ అవ్వాలి. లాగిన్ అయిన వెంటనే ఆధార్ నంబర్ ఎంటర్ చేయాలి. ఇష్టం అయితే నమోదు చేయవచ్చు లేదా తదుపరి అని పేర్కొన వచ్చు.

అనంతరం పాన్ నంబర్, ITR పేరు(ITR-1) అసెస్ మెంట్ సంవత్సరం సెలెక్ట్ చేసు కోవాలి. తరువాత ఇవ్వబడిన 3 ఆప్షన్ లు 1) పాన్ ఆధారంగా 2) గతంలో దాఖలు చేసిన రిటర్న్ ఆధారంగా 3) నూతన చిరునామా లలో ఒకటి ఎంపిక చేసుకొని లాగిన్ అవ్వాలి.

తదుపరి వచ్చే ఫారం లో వ్యక్తిగత వివరాలు, ఆదాయం వివరాలు, పన్ను వివరాలు, పన్ను చెల్లింపు వివరాలు, 80 G వివరాలు నమోదు చేయాలి. నమోదులు ఎప్పటి కప్పుడు సేవ్ చేసుకొంటే మంచిది. అన్ని నమోదులు పూర్తి అయిన తరువాత సబ్ మిట్ చేయాలి. 26 AS లో నమోదు అయిన పన్ను, ఇ- ఫైలింగ్ లో పన్ను ఒకే విధంగా ఉండాలి. లేనట్లయితే నోటీసులు వచ్చే అవకాశం ఉంటుంది.

ఎకనాలెడ్జ్మెంట్:

ITR- 1 సబ్ మిట్ చేసిన తరువాత ఎకనాలెడ్జ్మెంట్ ఆప్షన్స్ వస్తాయి. దానిలో 'NO CVC' అనే ఆప్షన్ ఎంపిక చేసుకొని తదుపరి వచ్చిన ఆప్షన్స్ లో 'Mobile OTP' ఆప్షన్ ఎంపిక చేసుకుంటే మన ఫోన్ కి, మెయిల్ కి OTP వస్తుంది. ఆ పాస్ వర్డ్ ని నమోదు చేస్తే ఎకనాలెడ్జ్మెంట్ మన మెయిల్ కి వస్తుంది. దాని నుండి ఎకనాలెడ్జ్మెంట్ డౌన్ లోడ్ చేసుకొని భద్ర పరచు కోవాలి. ఎకనాలెడ్జ్మెంట్ సీపిసి బెంగుళూరుకు పంప వలసినదీ, లేనిదీ ఎకనాలెడ్జ్మెంట్ క్రింది భాగంలో పేర్కొన బడుతుంది. పంప వలసి వస్తే సంతకం చేసి 3 నెలల లోపు పంపాలి.

పన్ను వర్తించే ఆదాయం రూ.2,50,000 కన్నా ఎక్కువ ఉన్న వారు జులై 31 లోగా

ఆదాయపు పన్ను రిటర్న్ దాఖలు చేయవలసి ఉంటుంది.

ఫిబ్రవరి మాసంలో సమర్పించిన ఫారం 16 ఆధారంగా రిటర్న్ దాఖలు చేయాలి.

దాఖలు చేయవలసిన విధానం:

వేతనం లేదా పింఛను ద్వారా ఆదాయం పొందుచున్న వారు, పెట్టుబడులపై వడ్డీ ఆదాయం పోన్స్య్ వారూ, ఒకే గృహం ద్వారా ఆదాయం ఉన్న వారు ITR-1(సహజ్) ఫారం ద్వారా రిటర్న్ దాఖలు చేయాలి.

ఆన్ లైన్ ద్వారా "ఇ- రిటర్న్" ను సులభంగా దాఖలు చేయ వచ్చు. దాఖలు చేసే విధానాన్ని పరిశీలిద్దాం.

పేరు రిజిస్టర్ చేసుకొనుట:

incometaxindiaefiling.gov.in వెబ్సైట్ ఓపెన్ చేసి Register your self అను ఆప్సన్ ను ఎంచుకొనవలెను. దానిలో పాస్ వర్డ్ తదితర వివరములను పూర్తిచేసిన తదుపరి మెయిల్ కు వచ్చిన లింక్ కాపీ చేసి బ్రౌజర్ లో పేస్ట్ చేసిన తర్వాత మొబైల్ కి వచ్చిన పిన్ నంబర్ ను నమోదు చేస్తే రెజిస్ట్రేషన్ పూర్తి అయినట్లే. మీ పాస్ వర్డ్ ను జాగ్రత్తగా ఉంచుకోవాలి.

ఫారం 26 AS:

ఇ- ఫైలింగ్ చేసేందుకు ఫారం 26 AS ను పరిశీలించుకోవాలి. పైన తెలిపిన వెబ్సైట్ ఓపెన్ చేసిన తదుపరి 'VIEW FORM 26 AS' ను ఎంచు కోవాలి. దానిలో యూజర్ ID అంటే పాన్ నంబర్, రిజిస్ట్రేషన్ లో మనం ఎంచుకొన్న పాస్ వర్డ్ తదితర అంశాలను నమోదు చేసిన తదుపరి ఫారం 26 AS ను క్లిక్ చేసి ఎసెస్మెంట్ సంవత్సరం సెలెక్ట్ చేసుకోవడం ద్వారా ఫారం 26 AS ఓపెన్ అవుతుంది. దానిలో ఆ సంవత్సరం మనం చెల్లించిన పన్ను సక్రమంగా నమోదు అయినదీ లేనిదీ పరిశీలించుకోవచ్చు. ఫారం లో పన్ను నమోదు సక్రమంగా ఉన్నప్పుడే ఇ- రిటర్న్ చేయాలి.

ఫారం 26 AS లో నమోదుల పరిశీలన:

ఫారం 26 AS లో మనం పరిశీలన చేసినప్పుడు మనం చెల్లించిన పన్ను సక్రమంగా నమోదు కానట్లయితే DDO కు తెలియజేయాలి. సక్రమంగా నమోదు కాక పోవడానికి కారణాలు DDO త్రై మాసిక రిటర్న్(Q1, Q2, Q3, Q4) లను సమర్పించక పోవడం లేదా సమర్పించిన వానిలో పొరబాటు జరగడం అయివుండ వచ్చు. త్రైమాసిక రిటర్న్ దాఖలు చేయవలసిన బాధ్యత DDO లదే కాబట్టి వారే దాఖలు చేయడం లేదా తప్పులను సవరించడం చేయవలసి ఉంటుంది.

ఇ- ఫైలింగ్ చేయడం:

ఫారం 26 AS లో పన్ను నమోదు సక్రమంగా ఉన్నట్లు సంతృప్తి చెందిన తరువాత ఇ- ఫైలింగ్ చేయడం ప్రారంభించాలి. ముందు చెప్పిన వెబ్సైట్ ఓపెన్ చేసిన తరువాత 'Quick e file ITR- 4S' ఎంపిక చేసుకోవాలి.

PAN నంబర్, పాస్ వర్డ్, పుట్టిన తేదీతడితర వివరాలను నమోదు చేసి లాగిన్ అవ్వాలి. లాగిన్ అయిన వెంటనే ఆధార్ నంబర్ ఎంటర్ చేయాలి. ఇష్టం అయితే నమోదు చేయవచ్చు లేదా తదుపరి అని పేర్కొన వచ్చు.

అనంతరం పాన్ నంబర్, ITR పేరు(ITR-1) అసెస్ మెంట్ సంవత్సరం సెలెక్ట్ చేసు కోవాలి. తరువాత ఇవ్వబడిన 3 ఆప్షన్ లు 1) పాన్ ఆధారంగా 2) గతంలో దాఖలు చేసిన రిటర్న్ ఆధారంగా 3) నూతన చిరునామా లలో ఒకటి ఎంపిక చేసుకొని లాగిన్ అవ్వాలి.

తదుపరి వచ్చే ఫారం లో వ్యక్తిగత వివరాలు, ఆదాయం వివరాలు, పన్ను వివరాలు, పన్ను చెల్లింపు వివరాలు, 80 G వివరాలు నమోదు చేయాలి. నమోదులు ఎప్పటి కప్పుడు సేవ్ చేసుకొంటే మంచిది. అన్ని నమోదులు పూర్తి అయిన తరువాత సబ్ మిట్ చేయాలి. 26 AS లో నమోదు అయిన పన్ను, ఇ- ఫైలింగ్ లో పన్ను ఒకే విధంగా ఉండాలి. లేనట్లయితే నోటీసులు వచ్చే అవకాశం ఉంటుంది.

ఎకనాలెడ్జ్మెంట్:

ITR- 1 సబ్ మిట్ చేసిన తరువాత ఎకనాలెడ్జ్మెంట్ ఆప్షన్స్ వస్తాయి. దానిలో 'NO CVC' అనే ఆప్షన్ ఎంపిక చేసుకొని తదుపరి వచ్చిన ఆప్షన్స్ లో 'Mobile OTP' ఆప్షన్ ఎంపిక చేసుకుంటే మన ఫోన్ కి, మెయిల్ కి OTP వస్తుంది. ఆ పాస్ వర్డ్ ని నమోదు చేస్తే ఎకనాలెడ్జ్మెంట్ మన మెయిల్ కి వస్తుంది. దాని నుండి ఎకనాలెడ్జ్మెంట్ డౌన్ లోడ్ చేసుకొని భద్ర పరచు కోవాలి. ఎకనాలెడ్జ్మెంట్ సీపిసి బెంగుళూరుకు పంప వలసినదీ, లేనిదీ ఎకనాలెడ్జ్మెంట్ క్రింది భాగంలో పేర్కొన బడుతుంది. పంప వలసి వస్తే సంతకం చేసి 3 నెలల లోపు పంపాలి.